Hermès Constance vs Birkin: Which Is the Better Investment?

A direct secondary market comparison — premiums, liquidity, access strategy, and whether the Constance's easier retail access makes it a viable Birkin alternative for investment-minded buyers in 2026.

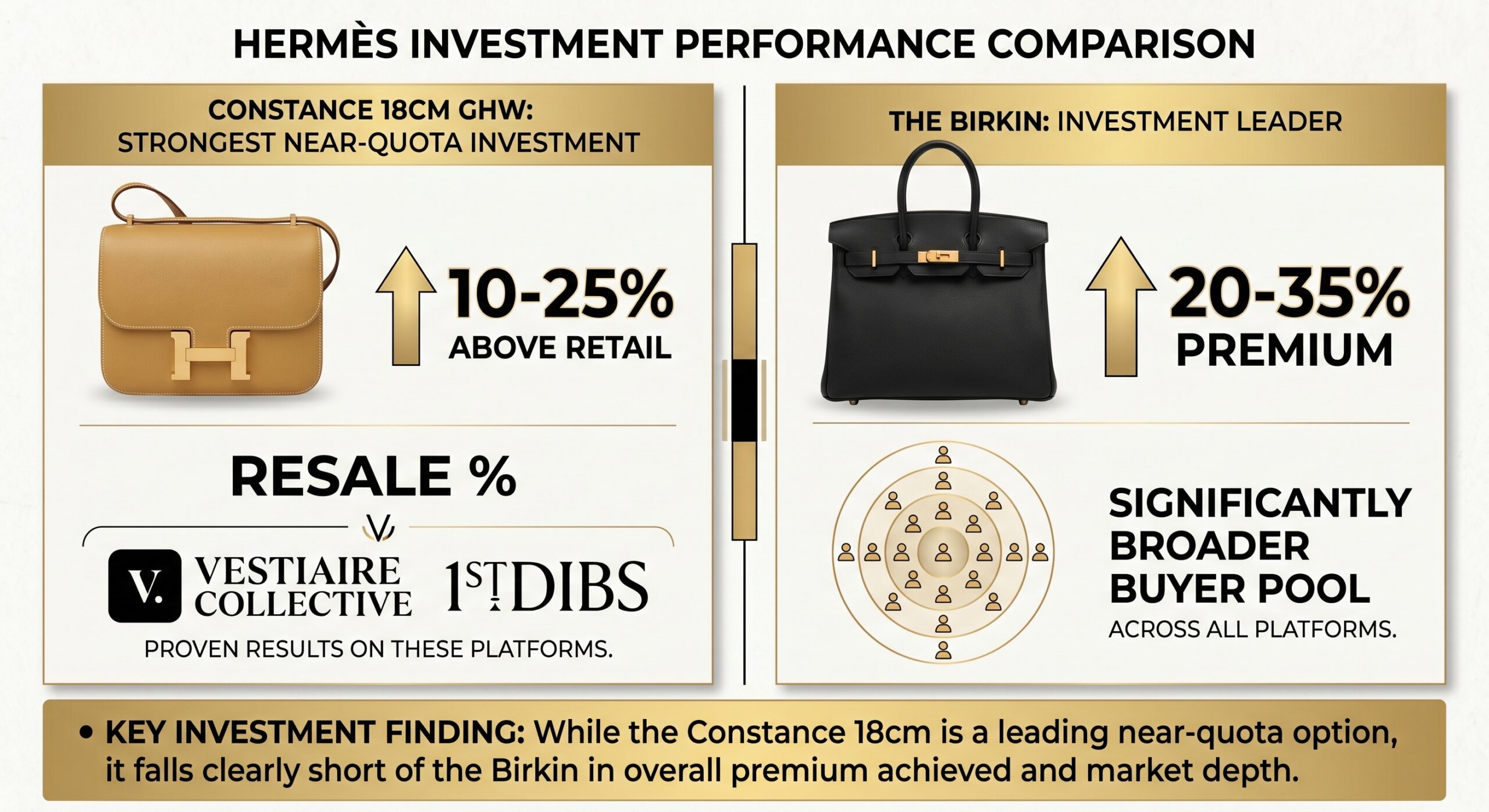

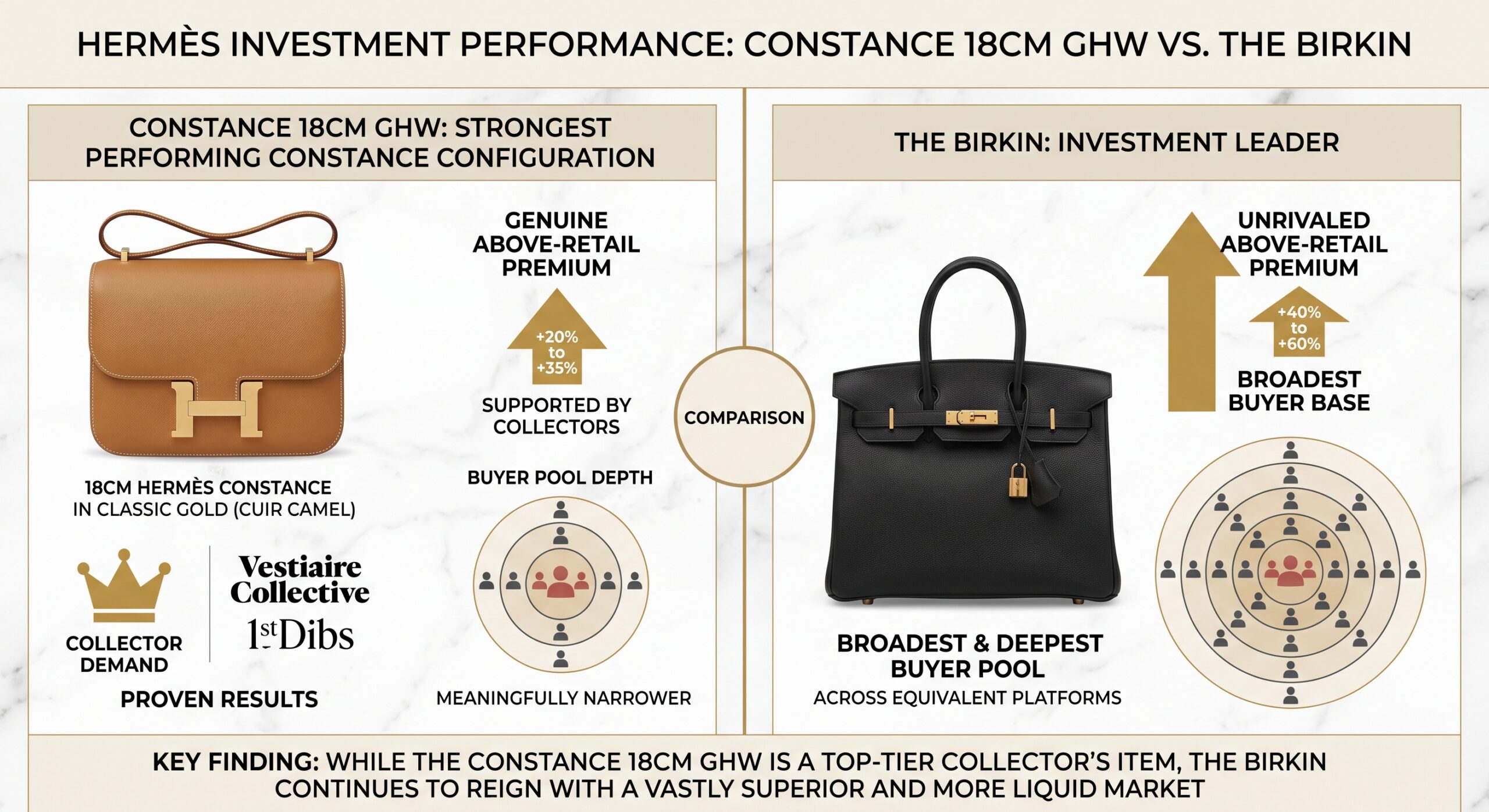

The Hermès Constance 18cm in gold hardware listed on Vestiaire Collective in excellent condition achieves approximately 10–25% above retail — a genuine secondary market premium that the Evelyne, Picotin, and Lindy cannot approach. The Birkin 30 in equivalent condition achieves 20–35% above retail. That gap defines the investment comparison between these two styles more precisely than any other single data point: the Constance is the strongest near-quota investment in the Hermès range, and the Birkin is the benchmark against which it should be measured — not against non-quota bags where the Constance always wins.

The Constance occupies a unique position in the Hermès investment hierarchy. It is technically available without the full quota bag boutique relationship that the Birkin requires — in some markets and boutiques, a Constance purchase requires less established spend history. But it consistently trades above retail on the secondary market, unlike the freely purchasable non-quota styles. It sits between tiers: not a quota bag with the Birkin's structural supply constraint and premium, but not a non-quota bag with no secondary market upside either. Understanding exactly where it sits — and when that middle position serves an investment strategy — is what this article delivers.

The Investment Framework: Quota vs Near-Quota

The fundamental investment distinction between the Birkin and the Constance is structural: the Birkin is a quota bag — accessible only through an established SA relationship and spend history — while the Constance occupies a hybrid position that varies by market. In some boutiques in some markets, a Constance can be purchased by a client with a relatively modest purchase history; in others, particularly in competitive flagship locations, the Constance has effectively become semi-quota — requiring meaningful relationship investment before allocation. The full comparison framework is covered in the Hermès Bag Comparisons Hub.

This structural difference has two investment implications. First, the Birkin's supply constraint at retail is more absolute and more consistent across markets than the Constance's — which is why the Birkin's secondary market premium is higher and more stable. Second, the Constance's variable access dynamics mean that in markets where it is more freely available, its secondary market premium reflects buyer demand for a distinctive Hermès piece rather than a scarcity premium. Where the Constance is genuinely restricted, its premium approaches the lower end of quota bag territory; where it is freely available, it trades closer to retail.

The Constance's above-retail secondary market position is not driven by supply scarcity in the way the Birkin's is. It is driven by three distinct demand factors. First, the Constance's distinctive flap closure and signature H-clasp design has an iconic Hermès visual identity that creates genuine collector appeal beyond the brand's broader product range. Second, the 18cm size is compact enough to read as a collector piece rather than a utility bag — a designation that supports premium pricing on platforms with strong collector buyer pools. Third, the gold hardware version has stronger collector demand than any other Constance hardware specification, reflecting the historical association between the Constance and the classic Hermès aesthetic.

Remove any of these three factors — try the Constance in standard hardware on a less collector-oriented platform, or in a non-18cm size — and the above-retail premium narrows considerably. The Constance's investment case is configuration-specific in a way the Birkin's is not.

The investment hierarchy within the Hermès range — from the Birkin at the top through the Kelly, the Constance, and the non-quota styles — is covered in our analysis of which Hermès bag styles hold their resale value best in 2026. The Constance's position in this hierarchy is consistently above all non-quota styles and consistently below the quota bag tier in premium percentage — a middle ground that makes it strategically valuable in some portfolio contexts while not substituting for the Birkin as an investment vehicle.

The Birkin's Investment Advantages

The Birkin outperforms the Constance on four of the five primary investment metrics: premium percentage, liquidity, buyer pool breadth, and correction resilience. Only on retail access difficulty does the Constance offer a structural advantage — and that advantage is partly offset by the fact that the Birkin's difficulty of access is precisely what drives its premium.

The liquidity advantage is the Birkin's most practically significant edge over the Constance. On Fashionphile and The Real Real — the two highest-volume Hermès resale platforms — Birkin transaction volume exceeds Constance volume by a substantial margin. The Constance's buyer pool is deeper and more engaged on Vestiaire Collective and 1stDibs, where international collector buyers seeking distinctive Hermès pieces browse actively. But on the volume platforms, Constance listings sit longer and command less competitive bidding than equivalent Birkin listings.

"The Birkin's buyer pool breadth advantage over the Constance is not a marginal difference — it reflects the fundamental distinction between a style that every serious Hermès secondary market buyer considers, and one that primarily appeals to a subset of collectors."

The five-year value retention comparison between the Birkin and Constance — covering the 2021–2026 period that included both the peak demand surge and the 2024–2025 correction — shows the Birkin maintaining premium leadership throughout. The Constance's correction was most visible in the 24cm size and in GHW configurations that had been bid up during the peak period; the 18cm GHW maintained a more resilient position. Even at its most resilient, the Constance's correction floor was lower than the Birkin 30's, confirming the structural premium advantage that quota bag status provides. Our companion analysis of Birkin vs Kelly value retention over five years provides the full five-year context that frames this Constance comparison.

- Always prioritise Birkin allocation over Constance acquisition when your boutique relationship has progressed to a quota bag offer — the premium differential makes the choice clear on investment grounds.

- The Birkin's correction resilience advantage is configuration-specific: Birkin 25 and 30 held premiums best through the 2024–2025 period; the Constance 18cm GHW held reasonably well; the Constance 24cm corrected more significantly.

- Platform selection for Birkin exit is more flexible than for Constance exit — Birkin sellers can use all four platforms with reasonable confidence; Constance sellers achieve significantly better pricing on Vestiaire and 1stDibs than on Fashionphile or The Real Real.

The Constance Case: Where It Holds Its Ground

The Constance is not a weak investment by Hermès standards — it is simply not a Birkin. Against the non-quota tier (Evelyne, Picotin, Lindy), the Constance wins decisively. Against the quota bag tier (Birkin, Kelly), it does not. Understanding where the Constance holds its ground helps buyers use it correctly within a broader Hermès portfolio strategy.

The Constance 18cm GHW in excellent condition is genuinely defensible as a secondary market investment — not at Birkin premium levels, but at premium levels that clearly distinguish it from the non-quota tier. Its distinctive H-clasp silhouette and compact format appeal to a collector segment that views it as an underappreciated Hermès icon rather than a second-tier handbag. On 1stDibs, Constance 18cm pieces in excellent condition with original box and dustbag sell reliably to buyers who are specifically seeking the model rather than accepting it as a substitute for something else.

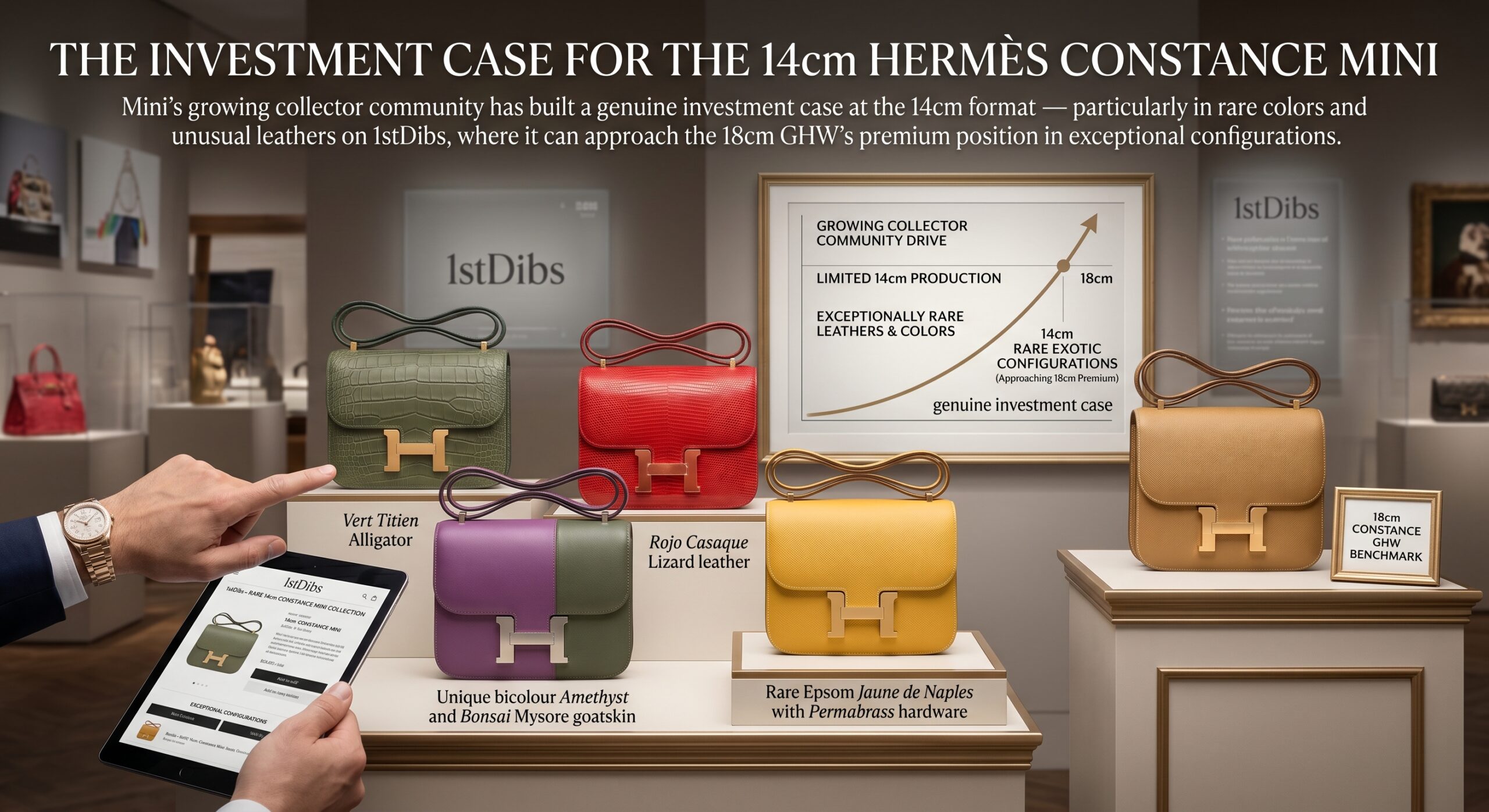

The Constance Mini (14cm) deserves specific mention for its developing investment case. Its collector community has grown significantly over the past two to three years — buyers who view the Mini as the most distilled expression of the Constance's design principles. In rare colors and unusual leathers on 1stDibs, Constance Mini pieces can command premiums that approach the 18cm GHW's position, and in the most exceptional configurations may exceed it. The Mini's investment case is not yet as stable as the 18cm GHW's — the collector community is newer and less predictable — but it is worth monitoring for buyers who acquire one through their boutique relationship. The design evolution of the Constance across its three sizes is explored by the team at Hermès Guidance Lounge's Constance design evolution guide, providing useful context on why the smaller sizes command stronger collector positioning.

There is one investment scenario where the Constance produces a superior outcome to the Birkin: when the Constance can be acquired at retail with minimal boutique relationship investment and the Birkin cannot yet be accessed. A buyer who is 6–12 months from qualifying for a Birkin offer but can purchase a Constance 18cm today at retail stands to generate a genuine 10–25% above-retail return from the Constance during the period they are still building toward their first Birkin allocation.

This scenario is most relevant in secondary or resort market boutiques where Constance access is relatively unencumbered, and least relevant in competitive flagship markets where even the Constance requires significant spend history. It treats the Constance as a temporary investment bridge rather than a permanent portfolio alternative to the Birkin — which is exactly the correct strategic framing.

The access advantage interacts with the Hermès fine jewellery comparison covered in our analysis of Hermès fine jewellery vs bag investment return — where jewellery serves a spend ratio function at a resale loss, the Constance serves a similar spend ratio function but with a positive resale position rather than a loss. Buying a Constance while building toward a Birkin allocation is more capital-efficient than buying jewellery for the same purpose, provided the Constance can be acquired at retail and resold above retail once the Birkin allocation arrives.

Portfolio Strategy: How to Use Both in an Acquisition Plan

The correct relationship between the Constance and the Birkin in an acquisition strategy is sequential rather than competitive: the Constance serves a bridge function during the relationship-building phase before Birkin access, and the Birkin is the destination investment once access is established. Treating them as investment alternatives rather than investment sequence components misframes the decision.

For buyers at early to mid stages of boutique relationship building — approximately months 3 to 12 — a Constance acquisition at retail serves three simultaneous functions: it adds to the global spend history that supports future Birkin allocation, it generates a positive resale position (unlike jewellery or non-quota bags), and it provides a lifestyle-appropriate Hermès piece to carry while the Birkin relationship matures. The investment efficiency of this approach — a Constance that returns 10–25% above retail versus jewellery that returns 70–90% of retail — makes the Constance the superior spend ratio tool among lifestyle-adjacent purchases.

- If your boutique relationship can access a Constance 18cm GHW at retail without requiring a full quota bag spend history, acquire it — it is the most capital-efficient relationship-building purchase available that also carries positive resale positioning.

- Do not delay a Birkin allocation to acquire a Constance instead — the premium differential makes the Birkin the correct priority whenever your SA relationship has progressed to quota bag offer territory.

- If offered a choice between a Constance and a Birkin in your SA relationship, always choose the Birkin — the investment case is not close enough to make the Constance a defensible alternative at equivalent retail access difficulty.

- For Constance pieces already in your collection, the correct exit platforms are Vestiaire Collective and 1stDibs — the collector buyer pool on these platforms provides the most competitive pricing environment for the Constance's distinctive positioning.

- The Constance's resale position improves meaningfully with full provenance: original dustbag, box, and authenticity card add approximately 5–10% to achieved price on Vestiaire and 1stDibs. Maintain documentation from purchase through to any eventual resale decision.

For buyers who have already built a Birkin or Kelly portfolio and are considering the Constance as a portfolio diversification: the 18cm GHW represents a defensible third acquisition that diversifies size and format without significantly diluting portfolio quality. Its correction profile differs from the Birkin's in ways that provide modest diversification benefit — a Constance that holds 10–25% above retail during a period when Birkin premiums are compressing still contributes positive absolute returns to the portfolio. It is not an investment-grade addition at the level of a second Birkin, but it is meaningfully better than any other non-quota diversification option. The full Market & Resale context is available through the Market & Resale category archive.

| Metric | Birkin 30 (PHW · Grade A) | Constance 18cm GHW (Exc.) | Constance 24cm (Exc.) | Winner |

|---|---|---|---|---|

| Secondary Market Premium | 20–35% above retail | 10–25% above retail | 8–18% above retail | Birkin |

| Liquidity (sell-through) | Fastest — all platforms | Moderate — collector | Moderate — slower | Birkin |

| Best Platform | All 4 platforms strong | Vestiaire · 1stDibs | Vestiaire Collective | Birkin (platform flexibility) |

| Buyer Pool | Broadest | Collector-focused | Narrower | Birkin |

| Correction Resilience | Strong (B30 held well) | Moderate (18cm held) | Weak (24cm compressed) | Birkin |

| Retail Access Difficulty | High (full SA required) | Moderate (market-dependent) | Moderate | Constance (access easier) |

| Spend Ratio Function | Primary investment vehicle | Best bridge purchase | Acceptable bridge | Constance 18cm (bridge role) |

| Overall Investment Verdict | Primary investment — always prioritise | Strong bridge — defensible third piece | Moderate — lower ceiling | Birkin |

Premium ranges are approximate and reflect observed secondary market outcomes for pieces in excellent condition with standard leathers. Rare colors, unusual leathers, and full provenance can significantly exceed shown ranges. Constance access difficulty varies significantly by market and boutique type.

Birkin Wins the Investment Comparison — Constance Wins the Access Comparison

The secondary market data produces a clear investment verdict: the Birkin 30 outperforms the Constance 18cm on premium percentage, liquidity, buyer pool breadth, platform flexibility, and correction resilience. The premium differential — 20–35% for the Birkin versus 10–25% for the Constance 18cm GHW — is meaningful enough to make the Birkin the unambiguous investment priority whenever both are accessible to a buyer at similar retail difficulty.

The Constance's one genuine competitive advantage is retail access in markets where it can be purchased with less boutique relationship investment than a Birkin requires. In those contexts, the Constance serves a legitimate and capital-efficient bridge function: it generates positive resale positioning, contributes to the global spend history that supports Birkin allocation, and provides lifestyle value during the relationship-building period. This bridge function is more valuable than any other comparable lifestyle purchase because it does not produce the resale loss that jewellery and non-quota bags generate.

Where the Constance fails is as an investment alternative to the Birkin for buyers who have the choice between the two. No collector-tier Constance configuration — not the 18cm GHW in rare color, not the Mini in exotic leather — reliably matches the Birkin 30's investment performance across a five-year holding horizon on a risk-adjusted basis. The Constance is the strongest non-quota-tier Hermès investment; it is not a quota bag substitute.

Bottom Line: Acquire a Constance 18cm GHW as a capital-efficient bridge investment while building toward Birkin access — then prioritise Birkin allocation at every opportunity once your SA relationship qualifies you for a quota bag offer.

Popular Searches

Explore our most searched Hermès Constance investment and comparison questions

Frequently Asked Questions

No — the Birkin delivers a stronger investment return than the Constance on every primary secondary market metric. The Birkin 30 trades at 20–35% above retail; the Constance 18cm GHW trades at approximately 10–25% above retail in excellent condition on Vestiaire Collective and 1stDibs. The Birkin's buyer pool is significantly broader, its sell-through speed is faster, and its premium retention through market corrections has been more resilient than the Constance's. The Constance is the strongest near-quota investment available — but it does not match Birkin-level returns. For the full quota bag investment hierarchy, see our analysis of which Hermès bag styles hold their resale value best in 2026.

The Constance 18cm in GHW is the strongest performing Constance size on the secondary market in 2026, achieving approximately 10–25% above retail in excellent condition on Vestiaire Collective and 1stDibs. The Constance 24cm achieves approximately 8–18% above retail. The Constance Mini (14cm) has developed a growing collector following and can command collector premiums on 1stDibs in rare colors or unusual leathers. Standard-sized Constance pieces in common configurations trade closer to retail on mainstream platforms and have lower liquidity than their Birkin counterparts.

The Constance's access dynamics vary by market. In some boutiques, the Constance can be purchased without the same spend ratio and relationship depth required for a quota bag — making it a more accessible retail acquisition. However, in competitive markets (Paris, Hong Kong, Tokyo, New York), the Constance in popular sizes and colors requires meaningful spend history and SA relationship before allocation. The access advantage over the Birkin is real but not universal. See our Birkin vs Kelly value retention analysis for how the Constance fits within the broader quota bag investment hierarchy.

For buyers whose primary objective is investment return, waiting for a Birkin is the correct strategy — the price-to-resale ratio differential between the Birkin 30 and the Constance 18cm is significant enough to make the wait worthwhile from a pure investment standpoint. For buyers who want an above-retail resale position with easier access than a Birkin and a genuine lifestyle benefit from ownership, the Constance 18cm GHW is a defensible choice — it is the only non-quota-tier Hermès bag that consistently delivers above-retail secondary market performance. The decision comes down to investment priority versus access timing.