Hermès Reseller Market Price Drop Analysis: 2024–2026 Trends

Which configurations corrected, which held firm, how each platform behaved differently — and what the 2024–2026 secondary market shift means for buyers and sellers navigating the market now.

Between late 2023 and mid-2025, the Hermès secondary market underwent its most significant premium compression since the post-financial crisis period — and most holders either misread it entirely or over-reacted to it. The correction was real: standard leather Birkin premiums above retail narrowed by approximately 8–18% from the 2022–2023 peak, with oversized formats and lower condition grade pieces bearing the sharpest adjustments. But the correction was not a collapse. Premium above retail was maintained across virtually all quota bag configurations throughout — the floor held precisely because Hermès retail price increases continued to rise during the same period, raising the reference point against which all secondary market premiums are calculated.

The reseller market price drop of 2024–2026 is best understood not as a failure of the Hermès investment thesis but as a normalisation from an exceptional peak. The 2021–2023 period saw secondary market premiums reach historically elevated levels driven by post-pandemic demand surge, constrained supply, and an influx of speculative buyers treating quota bags as short-term trading instruments. The 2024–2026 correction represented speculative demand unwinding and the market returning toward historical premium norms — not a structural reassessment of quota bag investment value.

This article gives you the full data picture: which configurations corrected most sharply, which held firm, how each of the four major resale platforms behaved differently during the correction, and what the current stabilisation means for buyers and sellers making decisions in 2026.

The Correction: What Actually Happened and Why

The 2024–2026 Hermès secondary market correction had three primary drivers, each operating simultaneously and reinforcing the others. Understanding all three is essential for evaluating whether current market conditions represent a buying opportunity, a selling window, or a hold signal — and the full investment framework is documented in the Hermès Investment Guide.

The first driver was speculative demand unwinding. The 2021–2023 period attracted a significant cohort of buyers who entered the Hermès secondary market primarily as short-term traders rather than collectors or long-term holders. These buyers bid premiums to historical highs, particularly in the most liquid standard configurations that offered the fastest exit. As broader luxury resale market conditions softened in 2024 — driven by macroeconomic pressure on discretionary spending and rising interest rates reducing the opportunity cost of holding cash — speculative buyers began exiting. Their sell orders landed on platforms simultaneously, increasing supply and putting downward pressure on ask prices.

The reason the Hermès secondary market correction did not become a collapse is structural: Hermès retail price increases continued throughout 2024 and 2025, raising the retail reference price against which all secondary market premiums are calculated. Even as premiums narrowed, the absolute dollar value of most quota bag positions held relatively stable because the floor kept rising.

A Birkin 30 that was trading at 35% above a $12,000 retail price ($16,200) in 2022 and saw its premium compress to 18% above retail in 2024 was still trading at approximately $15,340 — assuming retail had risen to $13,000 by that point. The premium compression in percentage terms looked dramatic; the absolute dollar movement was far more modest. This dynamic is why holders who understood the retail price increase mechanism were not alarmed by the 2024 correction, while holders who tracked only the premium percentage experienced significant anxiety over a much smaller real-terms change.

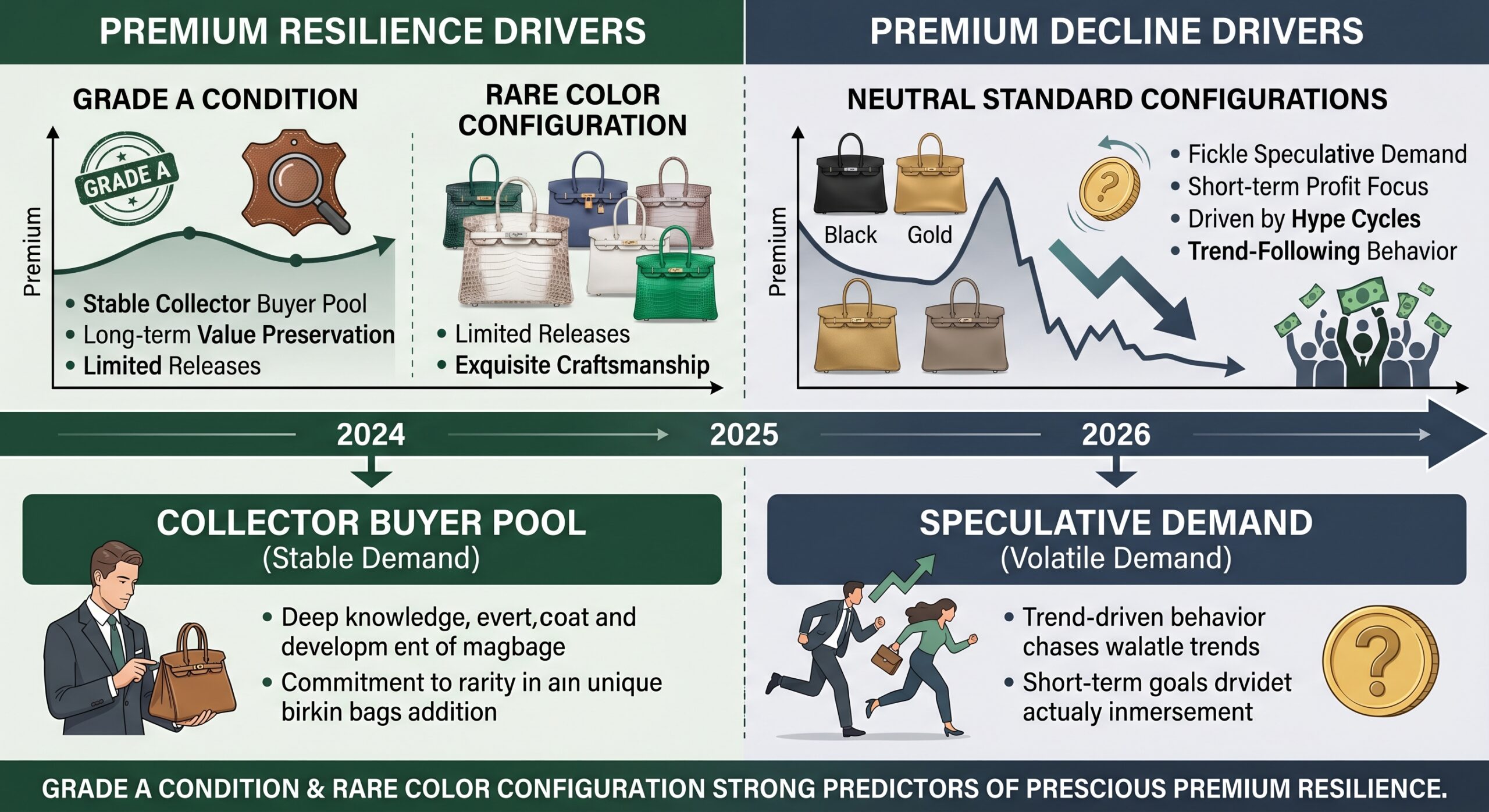

The second driver was condition grade normalisation. During the peak demand period, buyers accepted lower condition grade pieces at prices that would normally only apply to Grade A or Pristine examples. As the speculative cohort exited, buyers became more discriminating — grade B and B+ pieces that had briefly traded at near-Grade-A prices corrected back to appropriate condition discounts. This condition normalisation looked like a price drop but was actually the market returning to rational grading-based pricing.

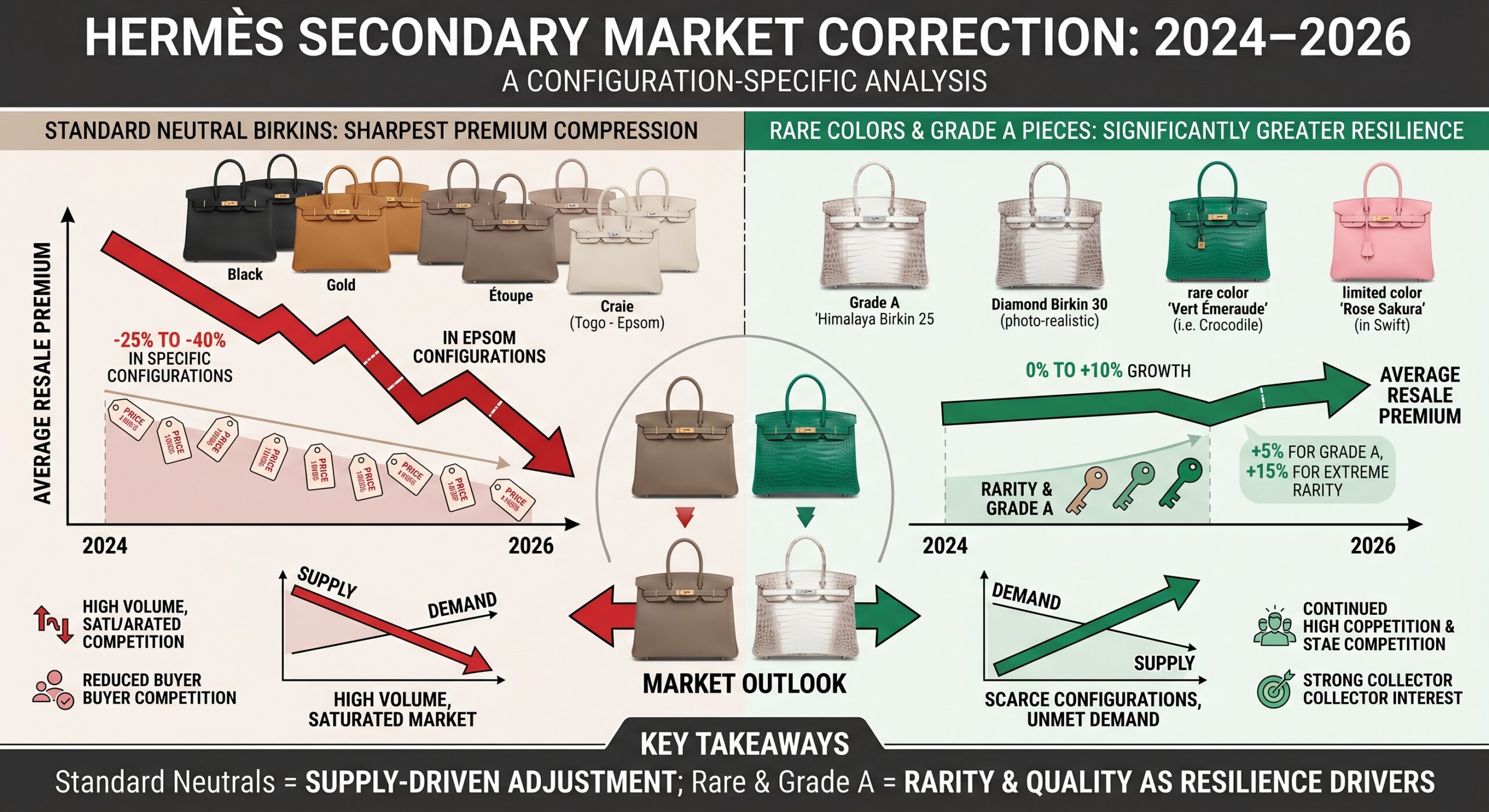

The third driver was the colour and format imbalance correction. Oversized Birkins — particularly the 35 and 40 — had seen disproportionate price appreciation during the peak, driven partly by speculation and partly by a brief trend-driven demand spike. As the trend reversed and speculative buyers exited, the 35 and 40 formats corrected more sharply than the 25 and 30, which maintained stronger demand from genuine collector and lifestyle buyers throughout.

What Held and What Corrected: Configuration Analysis

The correction's impact was not uniform across the Hermès secondary market. Understanding the specific configurations that demonstrated resilience versus those that bore the sharpest adjustments provides the intelligence needed for both buying and selling decisions in 2026.

The most striking finding in the configuration analysis is the divergence between the top and bottom of the market. While standard-grade, oversized, and neutral configurations saw meaningful premium compression, the collector tier — rare colors, Grade A small-format pieces, exotic leather HSS — actually strengthened during the same period. As speculative buyers exited the accessible tier of the market, serious collector capital concentrated into the configurations that are genuinely scarce and condition-consistent. This bifurcation is the dominant market structure in 2026.

"The 2024–2026 correction separated the Hermès secondary market into two distinct tiers: the speculative-demand-driven configurations that corrected, and the genuine collector configurations that held or strengthened. Knowing which tier your piece sits in determines everything about your current strategy."

The rare color resilience pattern is particularly significant for buyers making acquisition decisions today. Our companion analysis of Hermès rare colors that outperform on the resale market covers the specific shades that demonstrated the greatest premium resilience through the correction — and why the collector community's sustained demand for those colors created a floor that speculative selling pressure could not break. For buyers evaluating the current secondary market as an entry point, rare color Grade A pieces in the collector tier represent the most defensible acquisition position available.

- Grade A condition is the single most important variable for correction resilience — pieces that maintained top condition grade held premiums significantly better than equivalent configurations in B+ or below.

- Small formats (Birkin 25, Kelly 25) demonstrated greater resilience than large formats (Birkin 35/40) throughout the correction period — the collector demand pool for compact pieces is deeper and more stable than for oversized formats.

- Rare colors held better than neutrals — counterintuitive given that neutrals offer higher liquidity, but the collector specificity of rare color demand proved more stable than the broad-base demand for neutral configurations during the speculative exit.

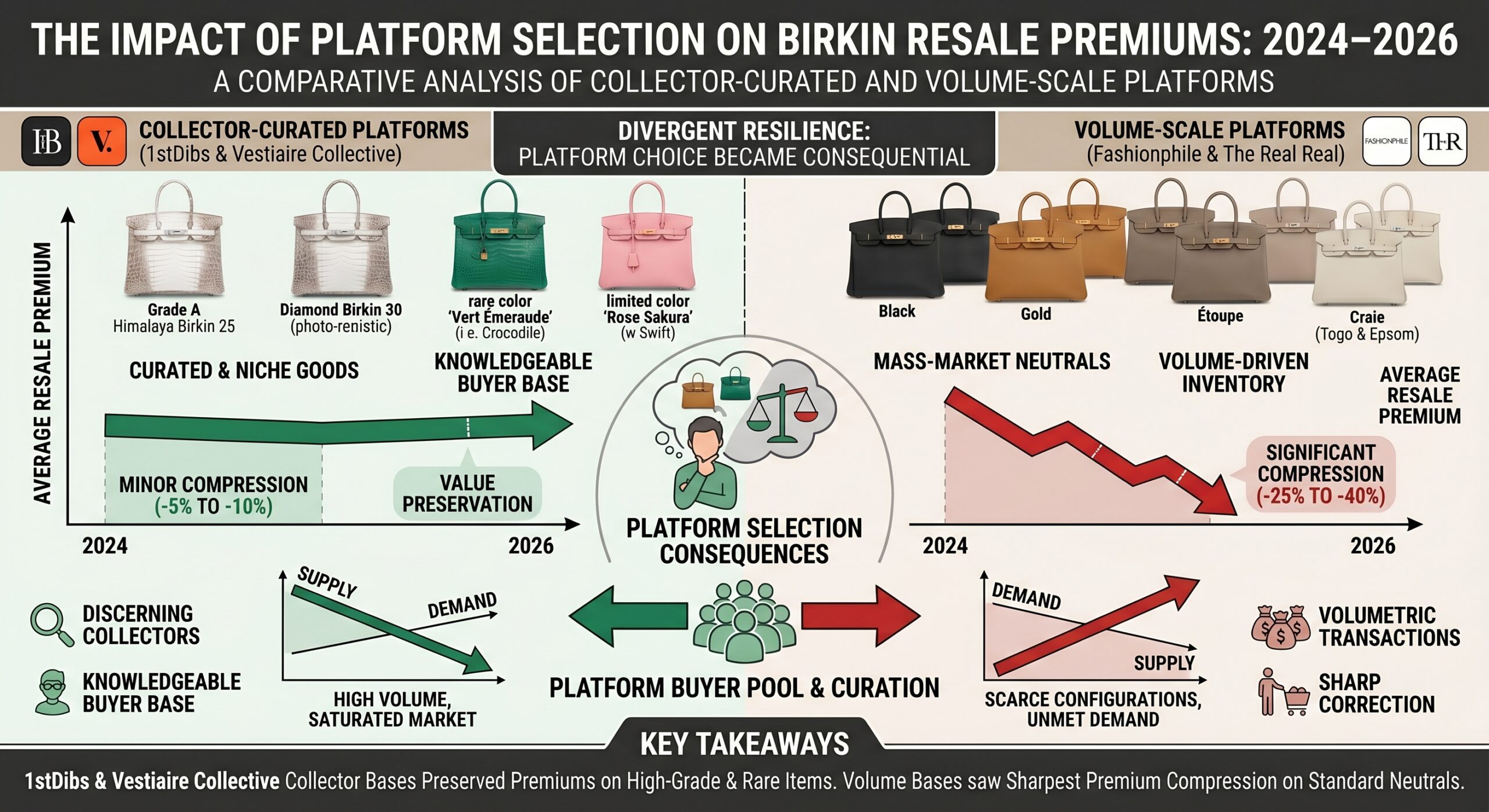

- Platform matters more during corrections than during rising markets — pieces listed on Vestiaire Collective and 1stDibs maintained stronger pricing than equivalent pieces on Fashionphile and The Real Real, as collector buyers anchored the international platforms while speculative seller supply concentrated on the volume platforms.

Platform-by-Platform: How Each Market Behaved

The four major resale platforms behaved distinctly during the 2024–2026 correction, reflecting their different buyer pool compositions, pricing mechanisms, and inventory management approaches. Understanding these differences is essential for sellers deciding where to list and buyers evaluating where to source.

1stDibs demonstrated the greatest premium resilience throughout the correction period. Its dealer-led model and high-spend collector buyer pool meant that speculative seller pressure — concentrated on the more accessible volume platforms — did not materially affect ask prices for top-tier pieces. Dealers on 1stDibs maintained their pricing discipline, and the collector buyers who anchor that platform continued purchasing at pre-correction levels for genuinely scarce configurations. The platform's correction was narrow and shallow relative to the broader market.

Vestiaire Collective showed more mixed behaviour — the platform's international buyer pool and seller-set pricing meant that speculative sellers could and did discount aggressively on standard configurations, while collector buyers sustained pricing on rare and exceptional pieces. The bifurcation between the collector tier and the standard tier was most visible on Vestiaire, where two pieces of the same model in the same leather could list at dramatically different premiums simultaneously depending on color and condition.

The Real Real bore the most visible correction pressure of any major platform. Its consumer-facing brand positioning and US-focused buyer pool had attracted the highest concentration of speculative buyers during the 2021–2023 peak — buyers who were treating quota bags as short-duration investments and were most sensitive to broader luxury market sentiment shifts. When those buyers began selling in 2024, The Real Real received the highest volume of corrective supply, and its pricing — set by the platform rather than individual sellers — adjusted downward fastest.

For buyers, The Real Real in 2024–2025 offered the most attractive entry points for standard configurations in good to excellent condition. For sellers during the same period, it was the weakest platform for maximising price on premium pieces — the consignment model's pricing algorithms reflected the platform-wide correction rather than the premium that individual rare pieces could command on Vestiaire or 1stDibs. The lesson for 2026: platform selection for the specific configuration and condition grade is more important than ever.

For colour-related analysis of which configurations showed the most dramatic premium divergence during the correction — and why certain shades acted as correction-resistant stores of value — the team at Hermès Guidance Lounge's colour resilience analysis provides the design-lens context that complements the investment data in this article.

Fashionphile occupied the middle ground during the correction. Its consignment model allowed for faster and more systematic repricing than Vestiaire's seller-set model, which meant it absorbed correction pressure more efficiently but also reflected that pressure more consistently across its inventory. Pieces submitted to Fashionphile during the peak of the correction received lower offers than equivalent pieces submitted six months earlier or later — a pattern that sellers who timed their submissions poorly experienced acutely. By mid-2025, Fashionphile's valuations had stabilised and begun recovering for top-tier configurations, while lower condition grade and oversized pieces remained at correction-level pricing.

2026 Market Position: Buyer and Seller Strategy

The 2026 Hermès secondary market is best characterised as post-correction stabilisation with selective recovery in the collector tier. The speculative excess of 2021–2023 has been largely cleared; the condition grade normalisation that the correction produced has largely completed; and ongoing Hermès retail price increases continue to support the floor beneath all secondary market pricing. The market is not back to 2022–2023 peak levels for standard configurations — and may not return to those levels without another demand shock — but it is no longer in active decline for any major configuration tier.

For buyers, the 2026 environment offers the most favourable entry conditions since 2020 for standard leather quota bag configurations. Premium compression has brought Birkin 30 and Kelly 28 pricing back toward historical norm levels relative to retail — buyers who waited through the peak are now able to acquire in configurations that were briefly inaccessible at rational prices. The key consideration is condition grade: the condition normalisation that occurred during the correction means that grade B and below pieces are correctly priced at meaningful discounts, and buying into those grades in hopes of recovery is not a sound strategy.

- For buyers: prioritise Grade A or Pristine pieces in the collector tier — the price premium over Grade B is justified by the resilience differential demonstrated during the 2024–2025 correction, and the recovery trajectory favours top-condition pieces most strongly.

- For sellers with Grade A standard configurations: the stabilisation in 2026 supports listing now rather than waiting for a full recovery to 2022–2023 peak levels — those peaks were driven by speculative demand that may not return at that scale.

- For sellers with rare color or exotic pieces in excellent condition: 1stDibs and Vestiaire Collective remain the strongest platforms — collector demand has recovered to near-peak levels for genuinely scarce configurations.

- For sellers with oversized formats (Birkin 35/40) or lower condition pieces: the correction in these categories has not yet fully resolved — patience or realistic price adjustment is required for successful exit.

- Platform selection in 2026: list collector-tier pieces on 1stDibs or Vestiaire; list standard configurations on Fashionphile for reliable sell-through; avoid The Real Real for premium piece sales until its recovery tracks more consistently.

The five-year value retention comparison between Birkin and Kelly — including how each style navigated the 2024–2026 correction — is covered in our dedicated analysis at Birkin vs Kelly: which holds its value better over five years. And for the retail price increase context that provided the floor beneath the correction, our Hermès price increase history analysis provides the complementary data set that explains why the floor held when speculative demand exited. The full secondary market intelligence archive is available through the Market & Resale category.

| Configuration | Peak Premium (2022–23) | Correction Depth | 2026 Position | Outlook |

|---|---|---|---|---|

| Birkin 25 — Togo/Epsom — PHW — Grade A | ~35–45% above retail | Shallow (−5–8%) | 28–38% above retail | Stable / Recovering |

| Birkin 30 — Togo/Epsom — PHW — Grade A | ~28–38% above retail | Moderate (−8–12%) | 20–28% above retail | Stabilised |

| Rare Colors (Rose Shocking, Bleu Electrique) — Grade A | ~38–50% above retail | Minimal (−3–6%) | 35–46% above retail | Strong / Recovering |

| Kelly 25 Sellier — Grade A | ~30–42% above retail | Shallow (−4–8%) | 25–36% above retail | Stable / Recovering |

| Birkin 30 — neutral — Grade B+ | ~22–30% above retail | Significant (−12–18%) | 10–16% above retail | Stabilised (slow recovery) |

| Birkin 35/40 — any leather — any condition | ~18–28% above retail | Deep (−15–22%) | 3–10% above retail | Soft / Uncertain |

| Non-quota styles (Evelyne, Picotin) — peak pricing | 0–8% above retail (brief) | Full reversal | At or below retail | Structural — no recovery expected |

| Exotic leather — Grade A — GHW — any size | Significant multiples | Minimal correction | Near-peak maintained | Collector demand stable |

Premium figures are approximate and reflect observed secondary market ranges relative to retail price. Currency movements, specific platform, and exact configuration affect actual outcomes. All data based on observed market patterns — not guaranteed future performance.

The Correction Is Over for Top-Tier Pieces — The Floor Is Higher Than Before

The Hermès secondary market price drop of 2024–2026 was real, configuration-specific, and now largely resolved at the collector tier. Standard Grade A Birkin 25 and 30 pieces, Kelly 25 Sellier, and rare color configurations in excellent condition have all stabilised or begun recovering their premium positions on Vestiaire Collective and 1stDibs. The speculative demand that drove the 2021–2023 peak has cleared, and what remains is genuine collector and lifestyle buyer demand — more stable, less excitable, and more discriminating about condition and configuration.

The critical insight for 2026 holders is the floor mechanism. Hermès retail price increases continued through the entire correction period, raising the retail reference price against which all secondary market premiums are calculated. A holder whose premium compressed from 35% to 22% above retail during the correction did not actually lose in absolute dollar terms if retail rose sufficiently during the same period — the floor moved up even as the premium percentage moved down. This is the dynamic that made the correction feel worse than it was for holders who tracked only the premium percentage.

The configuration hierarchy that emerged from the correction is the clearest signal for 2026 strategy: Grade A condition, small format, rare color, and exotic leather pieces demonstrated correction resilience that standard neutral large-format pieces did not. Building positions in the resilient tier — whether through boutique relationship allocation or secondary market acquisition at post-correction prices — is the most defensible quota bag investment stance available in 2026.

Bottom Line: The 2024–2026 Hermès secondary market correction normalised speculative excess without breaking the investment thesis — Grade A small-format and rare color quota bags have emerged from the correction with stronger relative positioning, and the retail price floor continues to rise beneath all secondary market pricing.

Popular Searches

Explore our most searched Hermès resale market and price trend questions

Frequently Asked Questions

Yes — the Hermès secondary market experienced a meaningful correction between 2024 and 2025, but the correction was highly configuration-specific. Standard leather Birkins and Kellys in neutral colors saw their premium above retail compress by approximately 8–18% from 2022–2023 peak levels. However, the correction did not push most quota bag configurations below retail — premiums narrowed rather than disappeared. Rare colors, exotic leathers, and top-tier collector configurations held their premiums significantly better than standard neutral configurations during the same period. The market correction was a repricing toward historical norms rather than a structural collapse. For the retail price context that provides the floor, see our Hermès price increase history analysis.

The configurations most affected by the 2024–2026 secondary market correction were: oversized Birkins (35 and 40) in standard leathers, which had been bid up most aggressively during the 2021–2023 surge; lower condition grade pieces (B and below) across all configurations; and non-quota styles that had briefly traded at premiums during the peak demand period. Standard Birkin 30 and Kelly 28 in Togo and Epsom with PHW corrected but retained premiums above retail. Rare colors in the blue, pink, and jewel-tone families showed the most resilient premium retention through the correction period.

In 2026, the Hermès secondary market shows signs of stabilisation rather than full recovery to 2022–2023 peak levels. Premium compression appears to have reached a floor for top-tier configurations — Birkin 25 and 30 in Grade A condition, Kelly 25 Sellier, and rare color pieces are all holding or modestly recovering their premium positions on Vestiaire Collective and 1stDibs. The broader luxury resale market correction that affected multiple categories in 2024–2025 has partially resolved, and serious collector demand has returned to the Hermès quota bag segment. See our Birkin vs Kelly five-year value retention analysis for the longer-term value retention context.

The sell-or-hold decision in 2026 depends primarily on three variables: your bag's condition grade, its configuration's position in the correction (whether it was heavily affected or relatively resilient), and whether continuing Hermès retail price increases are raising the floor faster than your premium is compressing. For Grade A Birkins in standard configurations, holding through the current stabilisation period is the stronger position — retail price increases continue to raise the floor, and the premium compression appears to have reached its trough for top-tier pieces. For lower condition grade or oversized configurations that were most heavily corrected, the calculus is less clear-cut.